In case you missed it, the Federal Housing Finance Agency (FHFA) granted conditional approval to Freddie Mac to purchase single-family closed-end second mortgages.

What this means is lenders will now be able to originate second mortgages and sell them off to one of the two government-sponsored enterprises (GSEs).

Arguably, this should improve access to such lending products, and potentially result in cost savings if increased competition drives down interest rates and fees.

At the same time, some have argued that this is inflationary (since it makes it easier for homeowners to take on more debt), while others have said it’s not part of the GSEs mission to boost homeownership.

I’m here to argue that this new pilot program is very limited and likely won’t change much, at least anytime soon.

What Is Freddie Mac’s New Second Mortgage Pilot Program?

In a nutshell, Freddie Mac is now permitted to purchase second mortgages that meet certain criteria.

As a result, there will be added liquidity in the lending markets for home equity loans, which are closed-end loans.

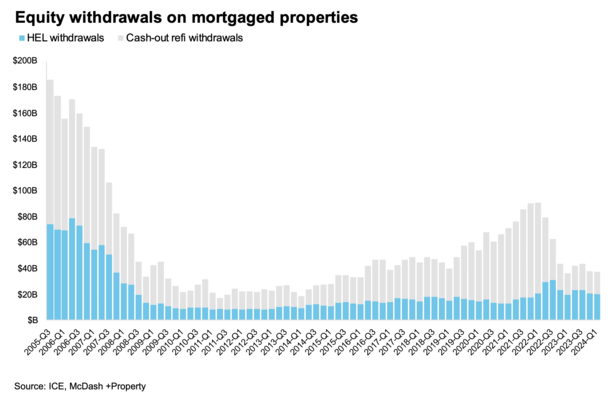

At the moment, most second liens, whether open-end HELOCs or closed-end home equity loans, are originated by large depository banks that typically keep them on their books.

The nonbanks often don’t have this luxury because it’s capital intensive, so the end result is that fewer mortgage companies offer such loans.

Notice the lack of home equity lending in the chart above provided by ICE, which has since been exacerbated by mortgage rate lock-in.

This can lead to negative outcomes for homeowners who might need access to their home equity to pay off other debt or fund purchases.

In fact, the pilot was approved by the FHFA to determine if the offering will advance Freddie Mac’s “statutory purposes” and benefits homeowners, especially those who reside in rural and underserved communities.

One of the arguments for the program is that HELOC providers often overlook lower-income homeowners in search of more affluent borrowers who open bigger lines of credit.

These happen to be more lucrative for those lenders since the larger the loan, the higher the commission generally.

Anyway, without getting too convoluted, the new program simply makes home equity loans easier to come by.

It’s not much different than the liquidity Freddie Mac (and sister Fannie Mae) provide for first mortgages, which makes them easier to obtain and cheaper too.

Who Qualifies for a Freddie Mac Second Mortgage?

While I myself was critical of this new program, mostly because you can already get a home equity loan from many different providers, there are several guardrails in place to keep this from becoming an unintended monster.

For one, it is limited to $2.5 billion in total loan volume over an 18-month pilot period.

This means once that money is exhausted, the program is closed and will be evaluated to determine if it should continue and/or be expanded.

In addition, the first mortgage must already be owned by Freddie Mac and the loan requires a minimum seasoning period of 24 months.

As such, a homeowner can’t get a Freddie Mac home equity loan unless they’ve had their existing first mortgage for at least two years.

And last but not least, it’s only available on primary residences and loan amounts are capped at $78,277.

This corresponds to subordinate-lien loan thresholds for Qualified Mortgages (QMs).

If you meet ALL these criteria, it may be possible to get a home equity loan behind your existing first mortgage that is backed by Freddie Mac.

Ideally, it will be easier to obtain and cheaper than other alternatives from private banks. But we don’t really know for sure.

This Program Is Going to Be Super Limited

As you can see from the program guidelines above, this isn’t going to be a massive program, at least not initially.

We know they won’t lend more than $2.5 billion, which broken down nationally isn’t a very large number.

For perspective, the nation’s largest second mortgage lender, PNC Bank, originated nearly 80,000 loans in 2022.

Assuming the typical loan is at the max loan amount of $78,277, it would result in less than 32,000 second mortgages being purchased by Freddie Mac.

Arguably it’ll be a lower average loan amount, but that still puts the loan count below that of just one provider.

In other words, it’s likely not going to make a big impact if the pilot doesn’t even generate as much activity as one other lender.

Especially when there are hundreds of other second mortgage providers out there.

But I’m sure everyone will be watching to see how it shakes out, and especially how the underwriting guidelines and mortgage rates compare.

Some also argue that this is just the beginning, and could usher in a full-blown second mortgage program backed by the likes of Freddie Mac AND Fannie Mae.

At which point everyone will be tapping equity left and right, potentially setting off another debt crisis (and eventual housing crisis).

But such worries are a long way away and not even founded at this juncture.

Home Equity Is at All-Time Highs While Withdrawals Are at Their Lows

As for why a program like this is necessary, the argument is to provide options for the underserved and an alternative to a cash out refinance.

The FHFA recognizes that with mortgage rates significantly higher today, refinancing the first mortgage in order to tap equity doesn’t make much sense.

And they know homeowners will do what they have to do if and when they need access to cash.

This could provide a lower-cost option versus a traditional refinance and also broaden participation of such lending to smaller, local shops instead of just big banks.

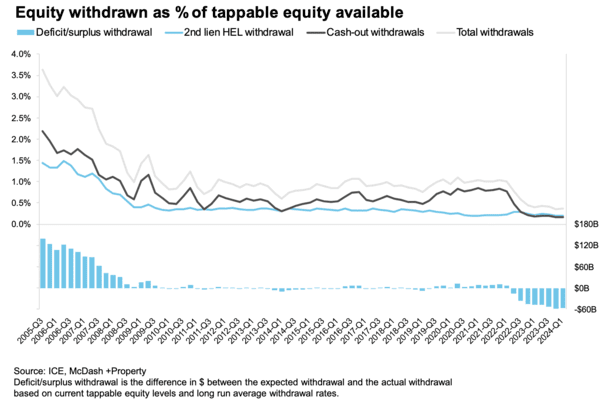

If you look at the latest stats, you’ll see that home equity withdrawals are rock bottom at a time when home equity has never been higher.

Per ICE, mortgage holders had a collective $16.9 trillion in equity entering the second quarter of 2024, of which $11 trillion could be tapped while maintaining an LTV of 80% or less. Those are both record highs.

Meanwhile, home equity withdrawals in the first quarter were equivalent to just 0.36% of tappable equity available, with both the fourth quarter of 2023 and Q1 2024 withdrawal rates the lowest on record (since 2005).

And about half of home equity withdrawal is happening via cash out refinancing, which likely isn’t ideal for borrowers with low fixed-rate first mortgages they lose in the process.

So we have an environment where home equity lending is already super low and a pilot that greatly limits how much can be generated via the program.

Of course, it is possible that the pilot pushes private lenders to up the ante and that leads to more home equity withdrawals, whether in the best interest of homeowners or not.